Quick answer: Car insurance for Indian immigrants in Canada is usually available once you have a valid licence, address, vehicle details, and payment method. Your first rate may feel high because many insurers do not fully count Indian driving history, but you can improve your quote by comparing providers, preparing proof of experience, choosing the right car, and understanding province rules.

You’ve just landed in Ontario with your Indian licence and no idea where to start. The car may be ready, the job may be far from transit, and every insurance quote may look higher than expected.

This page explains how car insurance for Indian immigrants in Canada works, why your Indian driving record may or may not help, and how to ask for a fair rate without guessing. You will also learn which documents to prepare, how province rules change the buying process, and what Ontario drivers should watch for from July 2026.

If you are still comparing licence rules, car costs, and insurance basics together, start with our main page on car insurance in Canada for Indians and then use this page to prepare your quote file.

As of April 2026, official sources such as Canada.ca and Ontario’s Financial Services Regulatory Authority explain that car insurance is required for vehicle owners, and Ontario insurers must use approved rating rules when offering auto insurance.

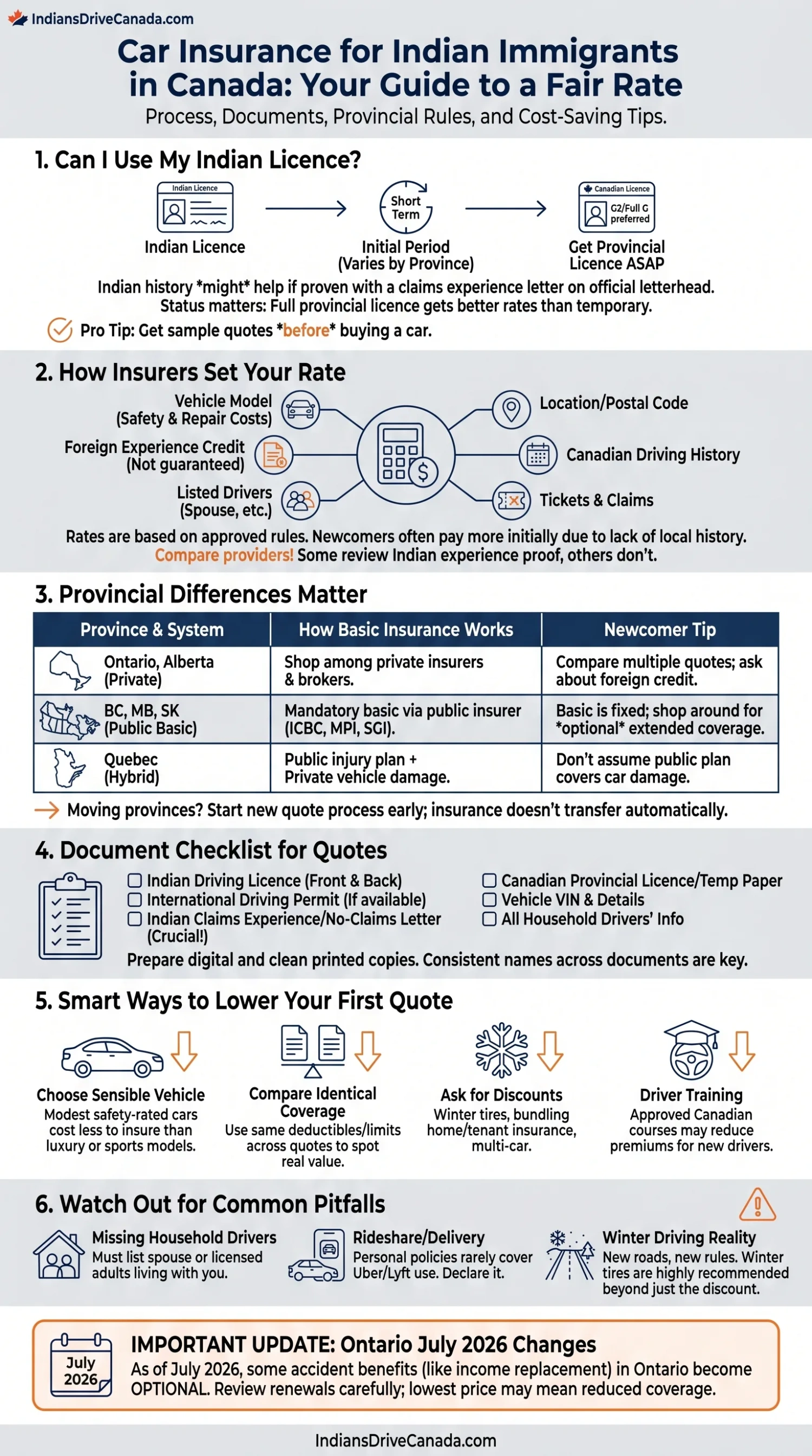

Can I Get Car Insurance in Canada With an Indian Licence?

Yes, but it depends on your province, your licence status, and the insurance company. Some insurers may quote you with a valid Indian licence for a short period after arrival. Others may ask for a Canadian provincial licence before they issue a policy.

Canada.ca tells newcomers that driving rules, licensing, and insurance are handled by each province or territory. That means Ontario, British Columbia, Alberta, Manitoba, and other provinces do not all follow the same process. You should check your local licensing rule before buying a car.

In Ontario, many newcomers first use their Indian licence for a limited time, then move through the DriveTest process. Insurers often prefer a G2 or full G licence because it fits their rating system more easily. A G1 licence can make insurance harder or more expensive because you cannot drive alone.

Your Indian driving history may still help if you can prove it clearly. Ask your Indian insurer for a claims experience letter. If possible, get it on company letterhead with your full name, policy dates, vehicle details, and claim history. Some Canadian insurers may consider it. Some will not.

DriveTest centres in Scarborough and Brampton have been known to see many newcomer licence-exchange questions, so booking early and carrying clean documents can save repeat visits.

Pro tip: Do not buy a car first and search for insurance later; get sample quotes before you sign any purchase or finance papers.

How Do Canadian Insurers Set a Fair Rate for Newcomers?

A fair rate does not always mean a cheap rate. It means the insurer uses approved rules, correct information, and the lowest rate available for your situation. In Ontario, FSRA says its role is to make sure proposed auto insurance rates are fair and not excessive.

Insurers may look at your age, Canadian licence class, years insured in Canada, address, vehicle model, commute distance, claims history, tickets, coverage limits, deductibles, and listed drivers. Newcomers often pay more at first because the insurer sees little Canadian driving or insurance history.

That does not mean you must accept the first quote. In Ontario, FSRA also says consumers can buy from an insurance company, agent, or broker, and should shop around before renewal. A broker can check several insurers. A direct insurer may be cheaper for some drivers. A comparison site may help you see the range.

Ask each provider the same questions:

- Will you review my Indian driving experience letter?

- Do you give credit for years licensed outside Canada?

- Would a Canadian driver training course reduce my premium?

- How much does the quote change with a higher deductible?

- Is usage-based insurance available for low-mileage driving?

Based on reports from Indian immigrants in Ontario forums, the biggest quote difference often comes from licence class, postal code, vehicle choice, and whether the insurer accepts any foreign experience proof.

Watch out: Never change your address, commute distance, or listed drivers just to lower a quote; wrong information can cause problems at claim time.

Which Province Changes the Way I Buy Car Insurance?

Car insurance for Indian immigrants in Canada changes a lot by province. The biggest difference is whether basic insurance comes from a public insurer, private companies, or a mixed system.

In British Columbia, basic coverage comes through ICBC. In Manitoba, basic Autopac comes through Manitoba Public Insurance. In Saskatchewan, basic plate insurance comes through SGI. In Quebec, injury coverage is handled through the public automobile insurance plan, while vehicle damage and civil liability are handled through private insurance.

In Ontario, Alberta, and most Atlantic provinces, you usually shop among private insurers, agents, and brokers. This can create a wide price range for the same driver. It also means comparing quotes matters more.

| Province | How Basic Insurance Works | Newcomer Tip | Official Link |

|---|---|---|---|

| Ontario | Private insurers, agents, and brokers | Compare several quotes and ask about foreign experience credit | FSRA auto insurance |

| British Columbia | Mandatory Basic Autoplan through ICBC | Ask an Autoplan broker about optional coverage | ICBC Basic Autoplan |

| Manitoba | Basic Autopac through MPI | Review deductibles and optional coverage before choosing | MPI insurance |

| Saskatchewan | Basic plate insurance through SGI | Extended coverage may still be needed | Saskatchewan auto coverage |

| Quebec | Public injury plan plus private vehicle coverage | Do not assume the public plan covers damage to your car | SAAQ public plan |

Pro tip: If you move provinces, your old insurance setup may not transfer cleanly, so start the new quote process before your move date.

What Documents Should Indian Immigrants Prepare Before Getting Quotes?

A clean document file can make the quote process faster. It can also help you prove that you are not a brand-new driver, even if you are new to Canada.

Prepare digital copies and printed copies where possible. Keep names consistent across documents. If your Indian licence uses initials, but your Canadian ID uses your full name, ask the insurer what proof they need to connect the records.

Useful documents include:

- Indian driving licence, front and back

- International Driving Permit, if you have one

- Canadian provincial licence or temporary licence paper

- Driving extract or licence history from India, if available

- No-claims or claims experience letter from your Indian insurer

- Canadian address proof

- Vehicle VIN, make, model, year, and trim

- Finance or lease details, if the car is not fully paid

- Names and licence details of all household drivers

Here is the exact process, step by step:

- Check your province licence rule before you test-drive or buy.

- Collect your Indian licence and insurance history documents.

- Choose two or three car models and get sample quotes for each.

- Ask one broker and two direct insurers for quotes on the same coverage.

- Review deductibles, liability limits, accident benefits, and optional coverage.

- Buy the policy before vehicle pickup, registration, or plate transfer.

The price can change quickly when you change the vehicle trim, postal code, annual kilometres, or deductible. For a financed car, the lender may also require collision and comprehensive coverage.

Watch out: A cheap quote with missing drivers or weak coverage may cost more later than a slightly higher quote that matches your real use.

How Can I Lower My First Car Insurance Quote in Canada?

Your first quote may feel unfair, but you still have practical ways to improve it. Start with the car. A modest sedan or small SUV with good safety ratings may cost less to insure than a luxury model, sports trim, or theft-targeted vehicle.

Canada.ca says insurers assign ratings based on claims made on different makes and models, and cars with better ratings can be cheaper to insure. So the car choice matters before you buy.

Next, compare coverage in a disciplined way. Use the same liability limit, deductible, drivers, address, and annual kilometres for every quote. If one quote is much lower, check what coverage was removed.

You can also ask about:

- Winter tire discount, where offered

- Bundling tenant or home insurance

- Usage-based insurance for careful, low-distance driving

- Higher deductible, if you can afford the claim cost

- Approved driver training course discounts

- Multi-car discount for family households

Real questions from Indian immigrants:

- “Will my 10 years of driving in India count?” Ask each insurer. Some may review proof, while others may not.

- “Should I buy the car in my spouse’s name?” Only if ownership, main driver, and payment details are true.

- “Can I insure before I get a full G licence?” Sometimes yes, but your rate and rules may differ.

- “Why did my Brampton quote differ from my friend’s Mississauga quote?” Postal code, car model, licence class, and history can all change pricing.

Pro tip: Get insurance quotes for the exact VIN before buying a used car, not just the make and model.

What Do Indian Newcomers Often Miss When Buying Insurance?

Many newcomers focus only on the monthly premium. That is normal when rent, deposits, furniture, and school fees are all arriving together. But car insurance has details that can affect your family budget after a claim.

The first missed detail is the listed driver rule. If your spouse, roommate, cousin, or adult child in the same home will drive the car, ask the insurer how to list them. Canada.ca says additional household drivers who may use the car should be listed on the policy.

The second missed detail is delivery and rideshare use. Personal auto insurance is not the same as commercial, delivery, or rideshare insurance. If you plan to drive for an app, tell the insurer before you start.

The third missed detail is winter driving. Winter tires may reduce risk and may qualify for a discount in some places. More than the discount, they help during snow, ice, and freezing rain.

New drivers from India also need time to adjust to local road habits. Four-way stops, school bus stopping rules, right turns on red where allowed, lane discipline, and winter braking distance can feel unfamiliar at first.

None of this means Indian drivers are unsafe. It means the first Canadian year has new rules, new roads, and new insurance language. Treat the first policy as something to review, not something to forget for 12 months.

Watch out: If your job, address, car use, or household drivers change, contact your insurer before renewal.

What Should Ontario Drivers Know About the July 2026 Insurance Change?

Ontario July 2026 update: FSRA states that as of July 2026, medical, rehabilitation, and attendant care benefits will remain mandatory, while other accident benefits will become optional. Ontario Regulation 383/24 also refers to optional benefits such as income replacement, non-earner, caregiver, death, and funeral benefits.

This matters for Indian immigrants in Ontario because the lowest monthly premium may not include benefits you expected. If you are the main earner, a student with part-time work, a spouse caring for children, or a newcomer without strong workplace benefits, review the optional benefits carefully.

Do not treat “optional” as “not needed.” It simply means you may have a choice. Ask your broker or insurer what is included by default, what was removed, and what each add-on costs per month.

Before renewing or buying an Ontario policy after July 1, 2026, ask:

- Is income replacement included or optional?

- Who in my household is covered by optional benefits?

- Are passengers covered in the same way as before?

- What changes must be confirmed in writing?

- How much do the optional benefits add to the monthly price?

As of April 2026, Ontario’s FSRA also explains that insurers must follow approved rules, and its Take-All-Comers guidance says eligible consumers should be offered the lowest rate available for their circumstances.

Pro tip: When comparing Ontario quotes after July 2026, compare benefits line by line, not only the final monthly payment.

Frequently asked questions

Can I Get Car Insurance in Canada With Only an Indian Driving Licence?

Sometimes, yes, but it depends on the province and insurer. Some companies may quote you during the short period when your Indian licence is accepted. Others may require a provincial Canadian licence before issuing a policy.

How Long Does Indian Driving Experience Count for Car Insurance in Canada?

There is no single Canada-wide rule. Some insurers may review an Indian insurer letter or driving history document, while others may give little or no credit. Always ask before accepting a quote.

Do I Need a No-Claims Letter From India?

It is not always required, but it can help. Ask your Indian insurer for a letter that shows your policy dates, claim history, and name exactly as shown on your licence or passport.

Can I Lower My Insurance by Taking a Driving Course in Canada?

Possibly. Some insurers may offer a discount for an approved driver training course, especially for newer Canadian drivers. Ask the insurer before paying for the course so you know whether it helps your quote.

What Happens if I Do Not List My Spouse as a Driver?

If your spouse lives with you and may drive the car, tell the insurer. Not listing a household driver can create claim problems. It may also make your quote inaccurate.

Can I Use the Cheapest Car Insurance Quote I Find Online?

You can, but check the coverage first. A cheaper quote may have a higher deductible, lower optional benefits, or missing drivers. Compare the same coverage before choosing.

Do I Need Different Insurance for Uber, Lyft, or Delivery Driving?

Yes, you may need special coverage. Personal car insurance may not cover rideshare or delivery work. Tell your insurer before using your car for paid driving.

What Happens if My Ontario Policy Renews After July 1, 2026?

Ontario accident benefit rules change from July 2026. Some benefits that were standard may become optional. Review your renewal documents and ask your broker or insurer what is included before you agree.